China’s laying hen industry reached a 5-year high in inventory in 2025, with average monthly birds in lay rising to 1.336 billion. However, weaker egg prices and oversupply pushed the sector into an average loss of CNY 12.79 per bird, despite lower feed and production costs. The report also highlights faster industry consolidation, shifting production regions, low processing rates, and stronger export growth for higher-value processed egg products.

China’s laying hen sector entered a more difficult phase in 2025, with flock expansion, weaker prices, and pressure on profitability all unfolding at the same time. A new report from the National Layer Industry Technology System said the country’s average monthly inventory of birds in lay reached 1.34 billion in 2025, the highest level in 5 years and around 77 million birds more than in 2024.

The report said the increase was driven by lower feed raw material costs in 2025, combined with the strong profitability cycle seen in the layer sector from 2021 to 2024. That encouraged companies to keep restocking aggressively.

“In 2025, China’s layer industry has entered a critical stage of deep adjustment and transformation,” the report said. It described a market shaped by faster scale expansion, more rational capacity reduction, ongoing technological change, and rising cost pressure, while the industry is also facing the difficult combination of high inventories and weak prices.

Imports of Grandparent Stock (GP) layers continued to decline last year. China imported around 127,000 GP birds in 2025, down 44% from 2024. Imported breeds mainly included Hy-Line, Dekalb Red, Hysex Pink, ISA, and Lohmann from France and Spain. Because of avian influenza in the United States, China did not import any GP layer breeders from the US in 2025. In 2024, by contrast, China imported 176,000 GP birds from the US, accounting for 77% of total imports.

Even so, production-level GP supply remained adequate. According to the report, China’s average monthly inventory of GP layers in production reached 539,300 sets in 2025, up 8% year on year. Domestic breeds accounted for nearly 73%, broadly unchanged from 2024.

Scale is also increasing. The report said 138 new layer projects were added in 2025, of which 81 were projects with more than 1 million birds, representing 69% of the total. Projects with more than 5 million birds reached 10.

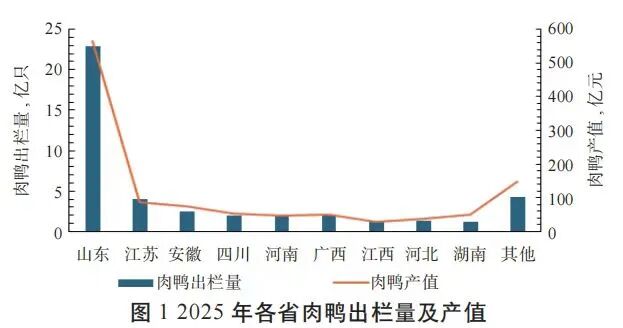

At the same time, the regional map of production is shifting. The traditional “eggs moving from north to south” pattern is weakening as new capacity moves south, expands in the east, and spreads west, blurring the line between production and consumption areas. In 2025, 9 provinces and municipalities — Guangdong, Hebei, Guangxi, Zhejiang, Hubei, Chongqing, Jiangxi, Henan, and Sichuan — each had planned capacity of more than 10 million birds, making them key growth areas for the sector.

That capacity expansion has added to market supply pressure. Although feed and production costs declined last year, with average production cost falling to CNY 150.31 per bird (USD 20.93), down 11.23% year on year, profitability still turned sharply lower in 2025. The average farming result for the year was a loss of CNY 12.79 per bird (USD 1.78).

The report said China’s laying hen inventory is now at a historical high, with supply pressure continuing to build and signs of periodic oversupply already visible. In that environment, it added, producers remain the core of the chain, but their weak ability to absorb market risk is becoming a major constraint on stable sector development.

Processing and trade

The report also pointed to another long-standing weakness: egg consumption in China still centers on shell eggs, while deep processing remains limited and value addition is low. In 2025, the country’s egg processing rate was just 14%, well below the 50% average seen in developed countries. That means processing has not yet played its potential role in absorbing surplus production or smoothing egg price swings, while innovation across the wider chain remains limited.

Product structure is part of the problem. Egg processing in China is still concentrated in traditional categories such as egg powder, preserved eggs, and salted eggs. Development of higher-end products, including functional egg products and egg-based food additives, has lagged behind. The report noted that profit margins for deeply processed egg products are significantly higher than for shell eggs, but outdated technology and the heavy investment needed for production lines make it difficult for smaller companies to enter the high-end segment.

The structure of the processing industry is also fragmented. Company concentration is low and most businesses are relatively small. Although egg products are one of the 3 major pillars of livestock products, the market capitalization of egg product companies remains below CNY 5.00 billion (USD 696.38 million), leaving a clear gap with meat and dairy processors. Most companies are still at an early stage of developing traditional products.

On exports, however, the structure is gradually changing from shell egg-led trade toward more processed products. In 2025, China exported 153,000 tonnes of shell eggs, up 9.5% year on year. Export value was USD 190 million, down 9.5%, while the average export price fell 17.3% to USD 1.2 per kg.

Exports of roughly processed egg products — including salted eggs, preserved eggs, and reprocessed eggs — reached 22,800 tonnes, up 1.4%. Export value was USD 60 million, down 0.6%, and the average export price fell 7.9% to USD 1.4 per kg, underlining the pricing pressure on lower value-added products.

More refined processed egg products, by contrast, performed much better. Exports of products such as liquid egg and egg powder reached 21,900 tonnes last year, up 35.6%. Export value rose 44.7% to USD 80 million, while the average export price increased 6.7% to USD 3.7 per kg. The report said these products provided important support to overall export performance.

Processed products are also becoming a more practical route into new markets. Hong Kong and Macao have long dominated China’s egg export trade, but the report said the industry is showing growing interest in expanding into Southeast Asia and the Middle East as regional trade ties deepen and overseas Chinese consumer markets grow. That is also pushing export structure toward a higher share of processed egg products, helping reduce transport risks and customs friction.

Problems and trends

According to the National Layer Industry Technology System, China’s layer industry covers the full chain, from breeding and farming to feed production, egg processing, logistics, and retail. But links across that chain remain loose, with overall coordination below 30%, which the report described as the core reason for the sector’s weak resilience.

In practice, upstream and downstream players still operate largely on their own, without effective mechanisms to share benefits and spread risk. The report said profit distribution across the industry is seriously unbalanced. When feed costs rise, feed companies pass the full pressure on to producers. When the market weakens, buyers push down purchase prices and transfer the risk, leaving producers to absorb the losses alone.

Vertical coordination also remains weak. Breeding and farming are disconnected, with breeding programs still focused too heavily on egg output while paying less attention to traits such as egg flavor and disease resistance. Feed formulation updates lag behind birds’ changing nutritional needs, reducing feed efficiency. At the same time, links between farming and processing are poor, creating a mismatch between deep-processing capacity and shell egg supply.

On the horizontal side, supporting services across the industry are still underdeveloped and third-party participation is limited. Distribution is also still dominated by traditional multi-layer trade channels, with too many links in the chain. That pushes losses to 8%–12%, far above the 3% level reported in developed countries.

Looking ahead, the system expects China’s egg prices to remain under pressure in 2026 as the market continues to face the combined squeeze of high feed costs and ample supply. Unless there is a major disease outbreak, extreme weather, or sharp volatility in raw material prices, egg prices are expected to fluctuate at relatively low levels within a range of CNY 5.50–8.00 per kg (USD 0.77–1.11 per kg), with only modest seasonal and holiday-related adjustments.

The report summed it up bluntly: the industry has moved into a phase of normalized low margins and competition within existing capacity. The era of making outsized profits from sudden market rallies, it said, has come to an end. For producers, more refined management is now the main way to offset market risk and keep operations sustainable.

AgriPost.CN – Your Second Brain in China’s Agri-food Industry, Empowering Global Collaborations in the Animal Protein Sector.