China’s 2025 meat duck output rose to 4.382 billion birds, but industry value fell as prices weakened and duckling prices dropped sharply. Exports and prepared duck products remained key bright spots.

China slaughtered 4.38 billion commercial meat ducks in 2025, up 3.86% from 2024, but total meat duck output value fell 9.61% year on year to CNY 116.01 billion (USD 16.16 billion).

That is according to a nationwide survey by the National Waterfowl Industry Technology System covering 23 major waterfowl-producing provinces, municipalities, and autonomous regions. Its newly released 2025 Waterfowl Industry and Technology Development Report shows a sector that kept expanding in volume, while value and pricing came under clear pressure.

East China remains the industry’s centre of gravity

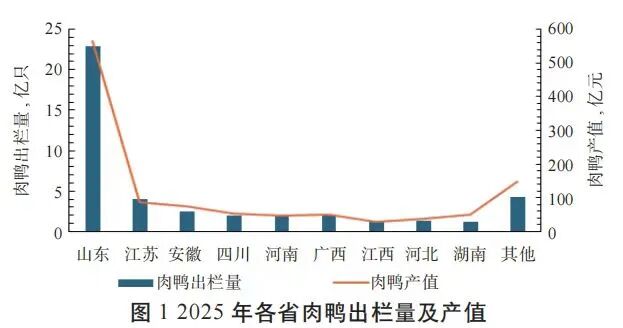

Production remains highly concentrated. East China accounted for 2.81 billion birds, or 71.91% of the national total.

At province level, Shandong remained the clear leader in both slaughter volume and output value, reaching 5.7 times and 6.5 times the level of Jiangsu, respectively. Jiangsu also moved past Guangxi and Anhui last year to rank second.

By breed, white-feathered meat ducks continued to dominate and increased their share further to 84.83%. Muscovy ducks and mule ducks accounted for 5.06%, while other breeds made up a combined 10.11%. Shandong remained focused mainly on white-feathered meat ducks, while Jilin, Fujian, and Guangdong were the main centres for Muscovy duck and mule duck production.

Lower prices, sharper swings

The report said the average live duck price in 2025 was CNY 7.60 per kg (USD 1.06 per kg), down 13.31% from 2024. The annual high was 36.09% above the annual low, underlining what the report described as a market marked by “a lower average level and intensified volatility”.

That pattern points to a market becoming more sensitive to slaughter timing, corporate procurement, and shifts in export demand.

Duckling prices were under even more pressure. The average duckling price in 2025 fell 51.72% from 2024, while the spread between the highest and lowest price during the year reached 363.64%.

According to the report, duckling prices trended upward from a low base, but swings remained extreme. That, it said, reflected sharply diverging expectations among producers, with cautious restocking and bouts of concentrated restocking both affecting supply stability.

Consumption shifts inland, exports gain momentum

On the consumption side, the system said demand in traditional markets such as East China and South China is moving closer to saturation. By contrast, second- and third-tier cities in Southwest and Central China are seeing continued demand growth, supported by the expansion of cold-chain logistics.

At the same time, prepared foods and ready-made meals are emerging as the main growth engine, with the industrialisation of foodservice accelerating penetration of pre-prepared duck products.

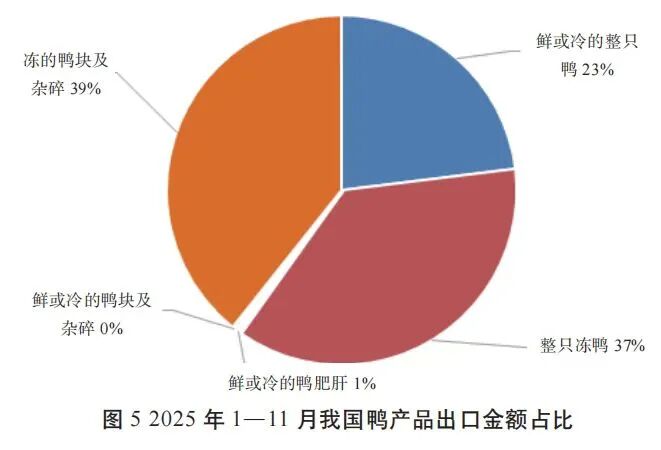

Exports also showed strong momentum, with shipment volumes rising quickly and export value increasing steadily. Frozen duck products and duck by-products were the main growth drivers.

From January to November 2025, exports of whole frozen ducks reached 54,800 tonnes, with export value at CNY 334 million (USD 46.52 million), up 95.45% and 41.67% year on year, respectively. Exports of frozen duck cuts and offal reached 42,700 tonnes, with export value at CNY 357.00 million (USD 49.72 million), up 86.68% and 41.67%, respectively.

Higher-value products also posted rapid growth. Exports of fresh or chilled duck foie gras rose 36.56% in volume and 59.71% in value from a year earlier.

The report said that performance suggests China has already built technological and quality advantages in some premium niche markets, while gradually forming a more diversified supply system spanning different duck product categories.

AgriPost.CN – Your Second Brain in China’s Agri-food Industry, Empowering Global Collaborations in the Animal Protein Sector.