Shennong Group has launched its second post-IPO equity incentive plan, granting 8.50 million restricted shares worth nearly CNY 300 million (over USD 40 Million) to 419 employees. Unlike its previous scheme, which focused on revenue and hog output growth, the 2025–2027 plan adds strict production cost ceilings to performance targets. Already among China’s most efficient hog producers, Shennong aims to cut all-in costs to CNY 12.00/kg (USD 1.67) by year-end through feed efficiency gains, disease prevention and supply chain optimisation.

On 29 July 2025, China’s Shennong Group – headquartered in Yunnan – unveiled its 2025 restricted stock incentive plan (draft), with a total market value of approximately CNY 295 million (USD 41.09 million).

The company will grant 8.50 million restricted shares, representing 1.62% of its total share capital, to 419 employees, including five directors and senior executives. The grant price is CNY 17.35 per share (USD 2.42 per share), compared to an average trading price of CNY 34.68 on the trading day before the announcement (USD 4.83 per share).

Among the recipients are vice presidents Dun Can (180,000 shares) and Zhang Xiaodong (150,000), board secretary Jiang Hong (130,000), employee director Sen Demin (80,000) and director Wang Ping (60,000). The remaining 414 middle managers and key staff will share 6.20 million shares, with 1.70 million (20%) reserved for future allocation.

Second plan since IPO

This is Shennong’s second equity incentive since listing in 2021, as Yunnan’s first agri-livestock listed company. In its 2022 scheme, the company granted 4.00 million shares to 184 employees – including the same three senior executives – with a market value of CNY 147 million (USD 20.47 million),and each of the three executives was initially slated to receive 100,000 shares.

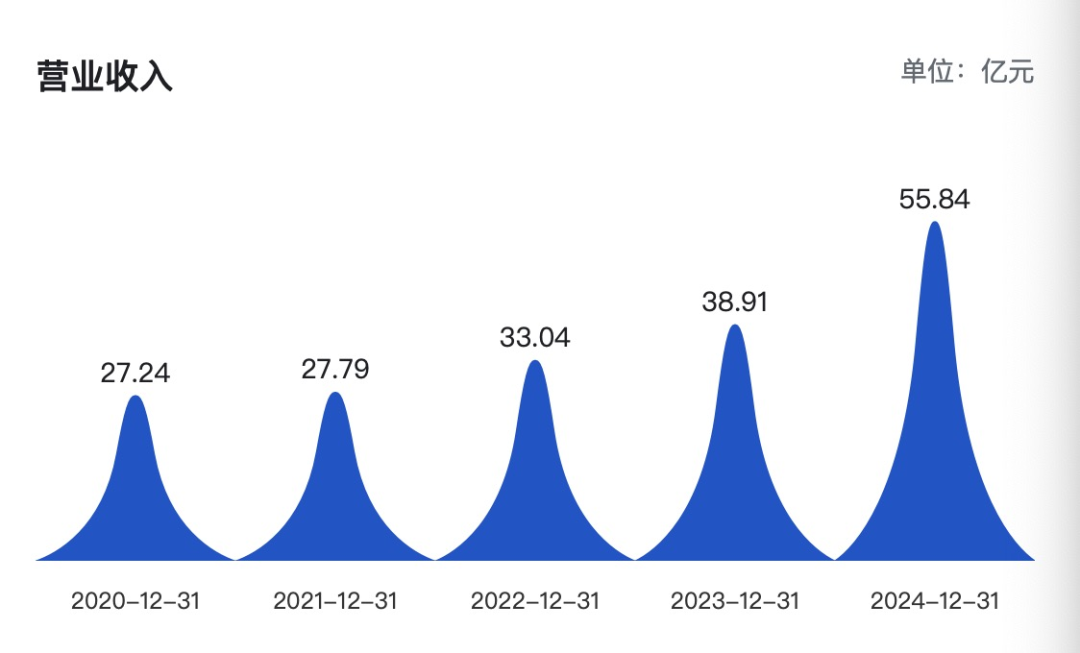

Shennong Group’s Revenue Growth Over the Past 5 Years

That earlier plan offered two performance routes: (1) annual revenue growth of at least 8%, 50% and 80% over 2022–2024, based on 2021; or (2) hog sales growth of 35%, 100% and 130% combined with slaughter growth of 10%, 20% and 30%.

Shennong met or exceeded nearly all targets. In 2022, revenue rose 18.89%, hog sales reached 929,000 head (+42.11%), and slaughter volumes grew to 1.44 million head (+10.63%). In 2023, hog sales climbed to 1.52 million head (+132.58% vs 2021) and slaughter volumes to 1.77 million (+35.22%), but revenue growth (40%) fell short of the 50% target, and the company recorded its first post-IPO loss – more than CNY 400 million (USD 55.71 million) – amid falling pork prices and higher feed costs.

By 2024, hog sales surged to 2.27 million head (+247.48%) and slaughter volumes remained 31.17% above 2021 levels. Revenue topped CNY 5.58 billion (USD 777.7 million), more than doubling the baseline year.

Under the 2025–2027 plan, (with 2024 as the base year) performance will hinge on either:

- Annual revenue growth of at least 10%, 24% and 64%; or

- Slaughter volume growth of at least 5%, 10% and 15%, while keeping all-in production costs below CNY 12.80/kg(USD 1.78 / kg), CNY 12.50/kg(USD 1.74 / kg) and CNY 12.20/kg (USD 1.70 / kg) respectively.

The new cost targets reflect Shennong’s focus on profitability in an industry prone to cyclical oversupply and volatile prices.

In the first half of 2025, Shennong’s all-in production cost was CNY 12.40/kg (USD 1.73), well below the sector average. According to AgriPost ,the company aims to reduce this further to CNY 12.00/kg (USD 1.67) by year-end, driven by improved feed conversion, better disease prevention and optimised supply chains.

AgriPost.CN – Your Second Brain in China’s Agri-food Industry, Empowering Global Collaborations in the Animal Protein Sector.