China’s pork industry is entering a phase of stability as government-led capacity controls and production efficiency gains reshape the market. While 2025 marks a cyclical downturn, piglet prices remain firm due to new demand sources. Dr. Wang Zuli highlights a shift toward lower profits but greater predictability in the world’s largest pig sector.

The era of sharp volatility in China’s pig farming industry—long dominated by pronounced “hog cycle”—appears to be fading. Dr. Wang Zuli, Chief Expert for Hog Industry Monitoring and Early Warning at China’s Ministry of Agriculture and Rural Affairs, stated at the inaugural High-Quality Swine Genetics Conference in Guangzhou that the market will enter a “micro-profit era,” with smaller price swings and improved long-term equilibrium.

Dr. Wang Zuli

“Under current regulatory frameworks, we won’t see unchecked expansion in breeding capacity. However, large-scale producers will also face challenges reducing their herds, as it would lower capacity utilization and increase costs,” Wang said. “This will likely result in a short-term stalemate in production levels. Unless disrupted by major events such as disease outbreaks, the wild price swings seen in the past 20 years are unlikely to return.”

Market Sentiment Still Drives Short-Term Fluctuations

Despite this newfound balance, market sentiment remains a significant influence on pricing. While China’s sow herd expansion in 2024 indicates that 2025 is a downcycle year, Dr.Wang emphasized that seasonal price rallies could still occur in the latter half of the year—provided market actors refrain from speculative hoarding or secondary fattening.

With production efficiency on the rise, the number of market hogs is expected to increase. “The state is actively guiding the reduction of overcapacity. For those enterprises with the means, trimming production would serve the long-term interests of the entire sector,” Dr.Wang noted.

Improved Efficiency Shrinks Demand for Breeding Stock

From 2013 to 2024, China’s breeding sow inventory declined by 11.23 million head—a 21.6% decrease—yet total pork production remained steady. This indicates a sharp improvement in production efficiency, driven by better genetics and increased average market weights.

“In 2007–2008, the average slaughter weight was around 106–107 kg. Today it has risen to about 130 kg,” Wang explained. “That’s a significant gain in productivity—pigs are simply growing faster to heavier weights at the same age.”

Meanwhile, pork consumption has plateaued. “In this context, demand for breeding stock may continue to decline. Alongside higher efficiency, we cannot rule out the possibility that pork consumption itself may begin to fall,” Dr.Wang said. “It’s time for the industry to reassess what a sustainable supply-demand relationship looks like.”

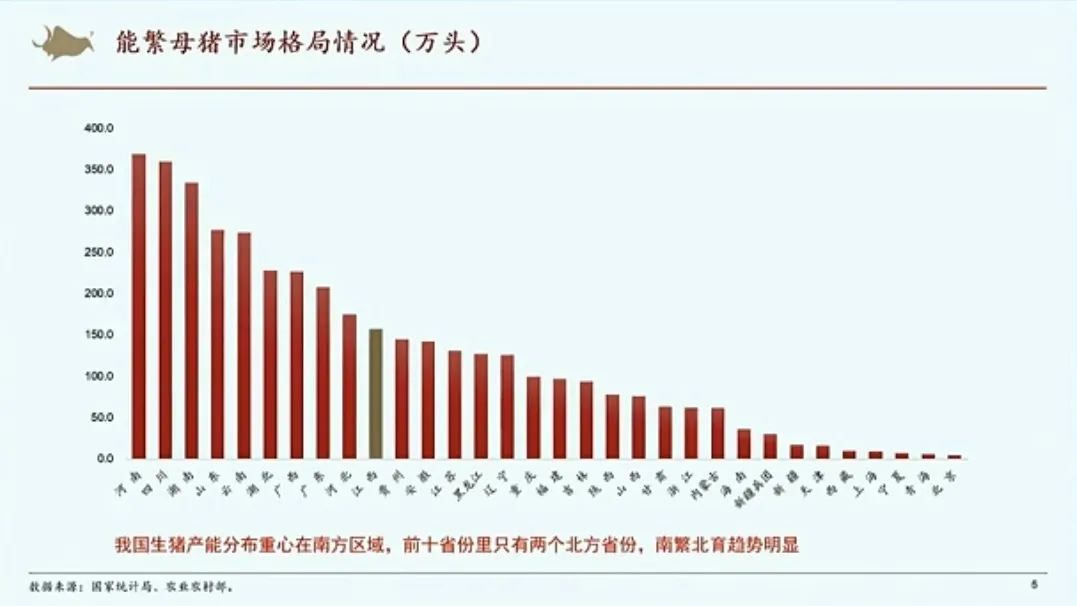

A Regional Shift: ‘Southern Breeding, Northern Finishing’

Another key transformation is geographic. Of the top ten provinces by breeding sow inventory, eight are located in southern China. This underscores the industry’s new post-ASF model: “southern breeding, northern finishing.”

Dr.Wang reiterated that swine price cycles remain ultimately driven by the sow herd cycle. Stabilizing sow inventory remains at the heart of state regulation. However, in the past two to three years, fluctuations in hog prices have far outpaced changes in F1 sow(hybrid sow)prices—highlighting the growing role of short-term speculation rather than long-term cycle investment.

Why Piglet Prices Remain Firm in a Downcycle

Although 2025 is structurally a downcycle year, piglet prices in the first few months of the year have remained unexpectedly strong—at times surpassing the per-head profits of market hogs. Dr.Wang attributes this to four key factors: bullish sentiment about future pork prices, seasonal restocking in early Q1, seasonal supply constraints due to wintertime disease, and above all, a shift in market composition.

New categories of buyers have emerged, including:

- Former backyard sow farmers who are now piglet purchasers;

- Rapidly expanding large-scale farms increasing external procurement;

- Small and mid-sized feed companies extending into downstream integration;

- Regional fattening platforms, particularly in provinces like Shandong.

Wang warned, “If any of these demand segments reverse, piglet price fluctuations could become even more pronounced than in past cycles.”

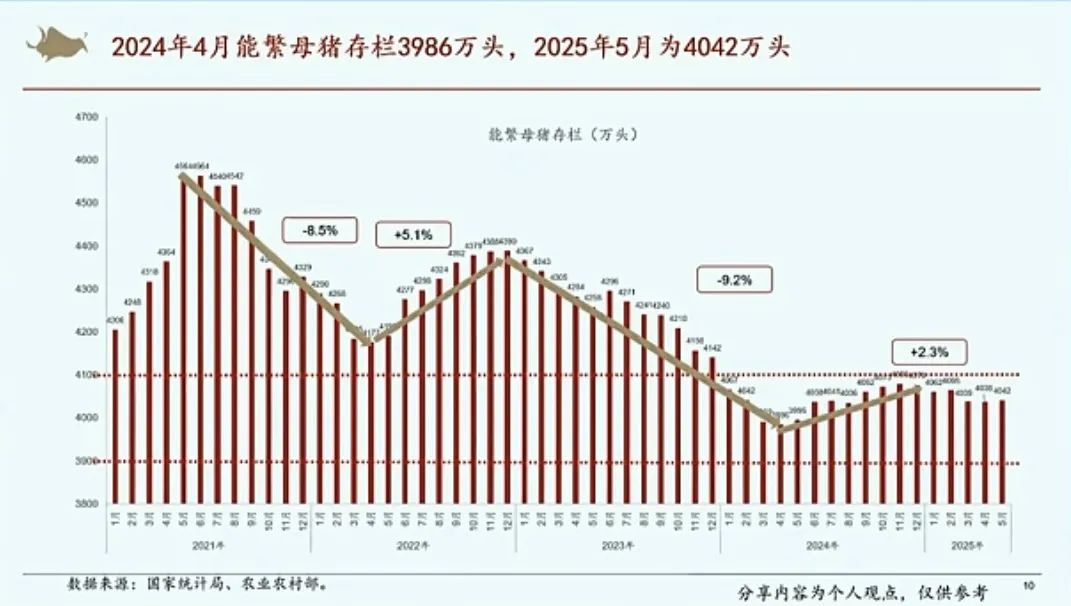

He also pointed out that while sow inventory rose steadily from April to December 2024, the net gain was only slightly above 2%, suggesting that the current year (2025) does not have the foundation for a sharp price collapse. “With sow numbers near the upper limit of the government’s green control range, sector-wide profitability will remain low.”

Domestic Demand Stable; Imports Minimal

Wang noted that pork consumption has remained relatively stable. In 2024, slaughter volumes fell approximately 3% year-on-year, while pork prices increased by 10%—a 1:3 elasticity typical of Chinese supply-demand dynamics.

“Consumption this year appears even stronger than in 2024,” he said. “In the first five months this year, both slaughter numbers and prices have risen—with slaughter growth outpacing price growth—this suggests firmer consumer demand is now supporting prices more than before.”

As for international trade, 2025 pork imports are expected to mirror 2024 levels, slightly exceeding 1 million tonnes. Imports thus account for just around 2% of China’s total pork consumption—rendering their impact on domestic prices marginal.

AgriPost.CN – Your Second Brain in China’s Agri-food Industry, Empowering Global Collaborations in the Animal Protein Sector.